"The power of independence is crucially important for those looking to combine content with sports betting"

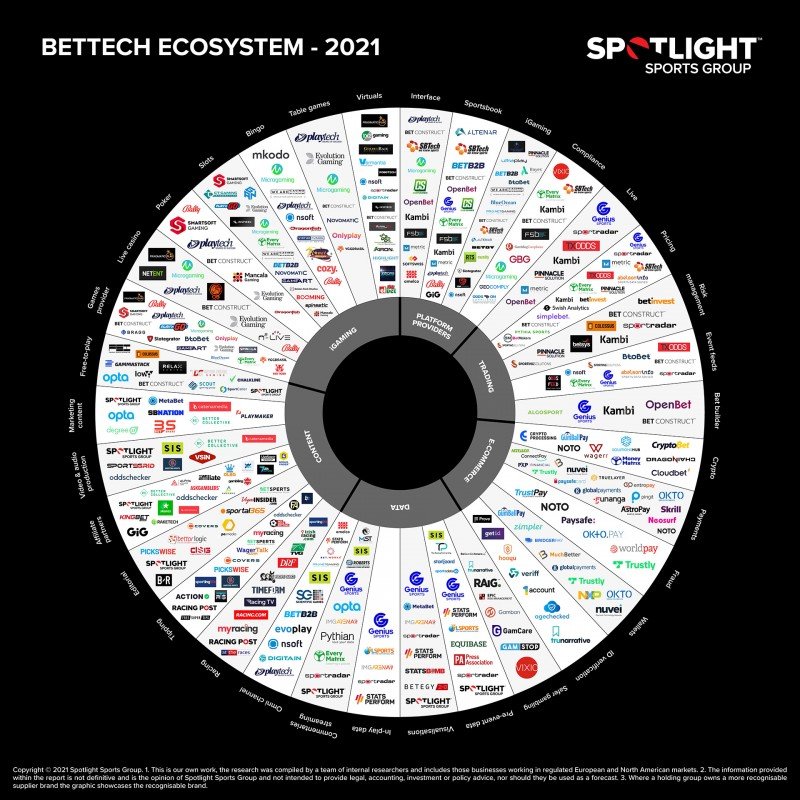

Spotlight Sports Group is a sports betting & DFS technology, content and media company that comprises Racing Post, MyRacing, Free Super Tips, and Pickswise in the US, has recently put together the BetTech Ecosystem, which aims to visualize the various sectors, sub-sectors and product specialists currently making up the complex sports betting industry.

Its key categories are Platform Providers, Trading and Ecommerce; Data and Content; and iGaming. In order to have first-hand insights into this comprehensive sports betting ecosystem and what this can tell us about the future of this market, Yogonet spoke with Harry von Behr, Managing Director (Sport) & US Co-CEO at Spotlight Sports Group. He notes the need for specialists driving innovation in the ecosystem, and he says the growth potential in the US is in the content section. Also, he sees iGaming and Casino becoming a bigger part of sportsbook strategy in the US alongside progressing the in-play offering.

The infographic of the BetTech Ecosystem produced by Spotlight Sports Group shows six main sectors and 34 subsectors. What were the criteria and approach to craft this kind of wheel, to decide each of the categories, and why have you decided to release it at this particular time?

We began by thinking if we were going to set up a sportsbook tomorrow what are the key elements we’d need to truly build a great betting experience. We then worked it from right to left as you can see on the visual with a platform of the first requirement followed by the other equally important segments.

We have worked on the research for quite a while and felt that was the best time of the year to release it, ahead of a number of key industry events (Sigma Malta and SBC Summit North America). Additionally, there has been a spike in M&A over the past few months and this research is a great tool for both those involved and to give an overview of the M&A activity that has taken place.

Which were the key learnings you have acquired in the process of making this ecosystem visualization and report? Could you share and further analyze some findings that stood out? How would you assess the synergies behind the different roles, segments and stakeholders, and where do you see growth potential?

What we wanted to do was shine a light on the variety of the sports betting industry. However, one of the main takeaways was the sheer size and speed that the market is moving at. What our research highlights are the wide range of companies that make up the ever-changing ecosystem. Businesses are constantly trying to grow via acquisitions and you can see from the visual how some businesses expanded to new sections from recent purchases.

The growth potential, especially in the US, is in the content section. It is obvious from some of the larger sportsbook deals we’ve seen that content is going to play crucial role in customer acquisition and retention strategies. The learnings from the European market is proof that this section will grow exponentially over the next few years.

Which role is diversification playing in this environment? Are you seeing a significant trend of companies with different core businesses and from other sectors becoming new players in the sports betting and iGaming industry? What was the impact of the pandemic and the shift towards digital in this sense?

Suppliers are definitely diversifying their portfolios, which is fairly plain to see from recent M&A activity. However, what we found really interesting is while you see the likes of Genius Sports or Sportsradar cover a huge segment of the industry (and the BetTech visual) there is a multitude of different businesses that specialize in one particular area. Whether that is iGaming and specific poker or slots providers, or on the payment side where we see a crossover with companies who work outside the industry. The ecosystem wouldn’t work with just three or four big businesses doing everything, there must be specialists driving innovation.

The pandemic, like with every industry, has played a huge role. The industry was heading digitally anyway but the closing of retail bookmakers in the UK and Europe and Casino and Sportsbook in the US has accelerated that transformation.

Amid several M&A going on, with major traditional operators trying to enhance their online offerings, do you still think we are facing a competitive and diversified market in the US? Or is there a significant risk that most of the market share eventually goes to the same few global firms, just under different brands?

The repeal of PASPA in the US created a once-in-a-lifetime regulated market opportunity. That combined with the sheer size of that market, versus the UK for example, has served as a catalyst for the growth of M&A activity. The range and quantity of start-ups, investors, operators, affiliates or content producers scanning the market for sports betting opportunities, investments or acquisitions is unprecedented and is not likely to slow down any time soon. The US is learning from the European experience, but the global nature of the sector’s leaders means European bettors will see improved customer journeys too.

It’s hard to predict where this stops but as we stated above there are a huge number of specialist businesses that make up our ecosystem that add significant value.

What's your view on the role gambling regulators and trade bodies are playing around this new ecosystem today?

Across the industry, representative bodies such as the BGC (Betting and Gaming Council) and RAIG (Responsible Affiliates in Gambling) have a keen focus on creating the safest possible gambling environment for consumers. The importance of safer gambling is showcased by multiple high-profile businesses working directly together to ensure players are protected.

The political pressure that has been building on operators in recent years is one reason why they must now show they are making efforts to reduce revenues from at-risk players and educate their customers about setting deposit and time limits. Aside from this outside pressure, the bulk of the industry now realizes it must provide a safer betting environment for its customers if it is to be sustainable.

How would you assess the affiliate market today, and its impact in this new sports betting scenario? What are your outlooks for affiliate resources?

As we have stated in the report - content very much remains king. On both sides of the Atlantic, our research shows that sports bettors place immense value in the integration of content within the product as the most compelling brand of sports betting content combines data, insights and opinions. This is what most affiliates strive to base their business models around.

The amount of traffic that is generated by affiliates remains a vitality important part of the ecosystem. Their corporate profile has also risen considerably in recent years and they play an active role in the high levels of M&A activity that we have seen so far, a trend that is likely to continue in the near future.”

Disney has recently announced a more aggressive approach to enter the sports betting market, via ESPN. This follows an increasing trend of media companies trying to capitalize this momentum in the US over the past few years. From your own perspective as a media brand, what is the differential factor, added value and specific competitive advantages of this kind of business profile? What are the keys to manage tailored content in a way that drives a flourishing business environment around sports betting, and attract the new player generations?

What is noticeable from the European market is the move away from sportsbook-supplied content to the super-affiliate models. In the mature markets that independent content offering is a market differentiator. While those sites have been acquired by some of the market’s biggest players, they’ve also lost their impartiality to an extent. Bettors may ask themselves if the content that they happen to be reading, from an ESPN Bet say, is benefiting themselves, or the platform.

Independent content is proven to create a more informed and confident bettor, our data shows that high-value bettors are in fact 50% more likely to read content before placing a bet. While 29% of high volume bettors (avg bet over $100) spend up to 3 hours researching bets. The power of independence is crucially important for those looking to combine content with sports betting.

Credible, independent content is a fundamental part of the customer journey in 2021, and it seems more pronounced in North America from our research. Providing that at scale is no mean feat and this is where third party solutions like Spotlight Sports group, flourish. It’s clear that scalable specialist content, from authoritative talent, is an extremely powerful combination for operators and publishers.

We are also seeing several funding rounds for startups successfully close, with a focus on sports betting. Which are the driving factors for investment in this ecosystem today, and which innovations and new players can we expect to see arise from this trend?

Every sportsbook operator has its own structural idiosyncrasies that will evolve per its own roadmap or the latest state opening. Bringing all that back to deliver a progressive customer proposition will remain a key challenge for years to come.

The supplier landscape evolves each month with each sportsbook looking to add that extra competitor edge and offer the best customer experience. We’re seeing iGaming and Casino becoming a bigger part of sportsbook strategy in the US alongside progressing the in-play offering. Those are probably the biggest growth area in the states. While Europe sees improved latency and 5G technology push the boundaries of live betting.

Wisconsin governor begins tribal talks to advance online sports betting rollout

Hard Rock Bet rolls out Matthew Broderick-led campaign for sportsbook and casino

Liga MX names Polymarket its exclusive prediction market partner for the US

Comtrade Gaming partners with 7bet for Latvia, Estonia and Finland expansion

1spin4win launches charity initiative 'United for Impact' to support children's healthcare in Kenya

Win Systems appoints Ana Aniceto to lead Country Manager & Sales in Peru

Flutter to delist from London on 3rd August as NYSE remains main trading venue

Ready Play Gaming content set to go live via Nirmata Play

Pidiots and the future of slot engagement: Why Slotmatic is building the intelligence layer behind the next generation of slots

BetMGM, Kaizen Gaming and Sportradar lead winners at SBC Awards Americas 2026

Boomerang Partners launches second stage of Golden Boomerang Awards 2026

Day 1 of SBC Summit Americas spotlights prediction markets, AI and industry challenges